- The OPEC+ Cuts of 9.7 million barrels per day (mbpd) held through June and are in place for July from last month’s extension. In a surprise, members more-or-less held to their promised cuts with Iraq, Nigeria and Russia complying. Russia, a reluctant cutter in the best of times, reached 9.3 mbpd, its target. Libya said that it is ready to lift force majeure at Es Sider oil port, allowing a tanker on standby to load crude from storage. Two smaller fields totaling about 0.4 mbpd were being restarted and expected to take three months to be at full production. With the opposition General Haftar in partial retreat, the possibility rose of a resumption of small exports of their high quality crude oil. Venezuela’s June oil exports were at a 77-year low of 379,000 bpd due to US sanctions – it even had to import gasoline from Iran as its refineries are effectively not working. Iran also still was trans-shipping oil through Malaysia to China in order to circumvent these sanctions as well. The next meeting on July 15th will determine whether the cuts will continue into August – given the potential production in the US and non-OPEC+ members, this seems likely. If they cannot agree on an extension, the cut will be reduced to 7.7 mbpd, a notable but not large increase. At around $40 per barrel in the US oil futures market, prices had gone as far as they can without a new catalyst.

- US Oil Production Fell Slightly from 11.2 mbpd of crude oil to 11.0 mbpd at the end of June with shale fields bearing the brunt of the 2020 production cuts. The US’

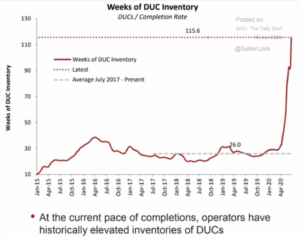

Energy Information Administration said it expects crude production will continue to decline until March, 2021, when output will average 10.6 mbpd and then begin rising again. It expects 2021 to have average production of 10.8 million bpd. US operating drilling rigs continued to fall, shifting from 222 on May 29th to 185 on July 3rd. It is too soon to say that the drilling rig count stabilized but there seemed to be light at the end of the tunnel. One item to watch will be the record number of Drilled, UnCompleted wells (DUCs – see right) which indicate production overhang on a demand recovery. Meanwhile the US has a record 540 million barrels of oil in storage – and increasing despite the summer driving period. A federal judge ordered the shutting of the Dakota Access PipeLine which transports much of that state’s Bakken shale oil production into the national pipeline system on environmental concerns. While running at reduced capacity due to the pandemic demand collapse, it will shift oil transportation to rail, which has its own problems. Also important will be following the energy-related bankruptcies, which included Chesapeake Energy on June 28th, and other write-offs, such as Royal Dutch Shell announcing up to $22 billion in assets. In another reduction, 10,000 employees of Brazil’s Petrobras, or 22% of its workforce, have accepted voluntary buyouts.

Energy Information Administration said it expects crude production will continue to decline until March, 2021, when output will average 10.6 mbpd and then begin rising again. It expects 2021 to have average production of 10.8 million bpd. US operating drilling rigs continued to fall, shifting from 222 on May 29th to 185 on July 3rd. It is too soon to say that the drilling rig count stabilized but there seemed to be light at the end of the tunnel. One item to watch will be the record number of Drilled, UnCompleted wells (DUCs – see right) which indicate production overhang on a demand recovery. Meanwhile the US has a record 540 million barrels of oil in storage – and increasing despite the summer driving period. A federal judge ordered the shutting of the Dakota Access PipeLine which transports much of that state’s Bakken shale oil production into the national pipeline system on environmental concerns. While running at reduced capacity due to the pandemic demand collapse, it will shift oil transportation to rail, which has its own problems. Also important will be following the energy-related bankruptcies, which included Chesapeake Energy on June 28th, and other write-offs, such as Royal Dutch Shell announcing up to $22 billion in assets. In another reduction, 10,000 employees of Brazil’s Petrobras, or 22% of its workforce, have accepted voluntary buyouts.

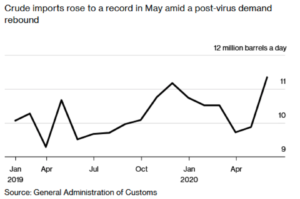

China Continued Driving Demand with estimates of oil imports hitting a record 11.9 mbpd on with strategic reserve buying and bargain hunting (+0.8 mbpd month-on-month and +2.4 mbpd year-on-year) – see the graph left. Even the US is getting a taste with China buying a record-high amount of nearly 1 million bpd for July. Crude stockpiles at 39 Chinese government and commercial storage sites monitored by Ursa Space Systems rose to 70% of capacity as purchases in the $20-range a few months ago were unloaded.

China Continued Driving Demand with estimates of oil imports hitting a record 11.9 mbpd on with strategic reserve buying and bargain hunting (+0.8 mbpd month-on-month and +2.4 mbpd year-on-year) – see the graph left. Even the US is getting a taste with China buying a record-high amount of nearly 1 million bpd for July. Crude stockpiles at 39 Chinese government and commercial storage sites monitored by Ursa Space Systems rose to 70% of capacity as purchases in the $20-range a few months ago were unloaded.

- China’s Reiterated Its Promise in mid-June to increase purchases of US farm goods – recall that China pledged to buy $36.5 billion worth of American agriculture products under the phase one deal, up from $24 billion in 2017, prior to the trade war. However, China purchased only $4.65 billion in the first four months of the year, per the USDA (13% of the promised amount). Soybean orders from the US picked up in June but lag. Meanwhile, soybean imports from Brazil soared in May to their highest in two years as backed-up cargoes that were delayed by bad weather in Brazil cleared customs. China brought in 8.86 tonnes of Brazilian soybeans in May, the highest since May 2018 and up 41% from last year’s 6.3 million tonnes. Brazil is expected to export 11.9 million tonnes of soybeans in June to China, pressuring American farmers. China’s hog production recovered further and was better than expected in May as pig inventories and the number of breeding sows continue to grow. While the US had shipped record amounts of pork earlier in the year, new records will be more challenging. Looking ahead in grains, US planned acreage for corn and soy surprised to downside but the crop looked healthy with the USDA rating 71% of the country’s corn and soybean crops in good-to-excellent condition at the end of June. Weather in July was forecasted to be hot, dampening yields but we do not see any pressing concern.

David Burkart, CFA

Coloma Capital Futures®, LLC

www.colomacapllc.com

Special contributor to aiSource