Uncertainty hit the equity markets in January as the tone of headlines turned slightly more negative. Weaker-than-expected US jobs growth caused hesitancy and the Federal Reserve continued its incremental reduction of the amount of debt it was buying, slowly removing its direct support from [artificially] low US interest rates. Bernanke and Yellen insisted that the Fed will not raise their benchmark overnight rate, thus extending the ZIRP as far as the eye can see (or at least for the next many months). Overseas, Europe and Asia continued their go-slow routine, with a number of emerging markets stumbling badly (Turkey, Argentina, Thailand, Libya, Ukraine) or making negative headlines (Russia, China, India, South Korea). Although each one by itself is not particularly important in the global scale of things (China being the obvious exception due to its GDP size and growth), some of these countries are important commodities producers or consumers and thus have an impact on markets. Positive sentiment points to the continuing shale revolution and low US energy costs, Iran and the West still negotiating and China having plenty of growth and cash to draw upon if needed. There is little if anything that is clear in today’s geopolitical and economic landscape so one must be flexible and open to possibilities.

{kind=link}

{kind=link}

Is a Glass Half-Full, Full Enough? Not if you are the S&P 500 and you just went up over 32%! A 3.5% loss in January has to hurt, though it is not even close to a standard correction of -10%. The economic data was generally mixed, with unexciting jobs numbers and slowing capital spending ending the year.  The Wall Street Journal put together this graphic comparison for the last seven years going to just before the recession in 2008. In January 2008, the US labor market reached its peak of just over 138.1 million workers on payrolls. It still has not returned to that level. Currently at 136.9 million, that number should be at 145.0 million to keep pace with population growth and to maintain the same labor force participation rate (see the graph on the right for the fall in the participation. The lower participation rate also has paradoxically improved the unemployment rate by lowering its denominator as seen in the middle graph). Capital spending for 2014 by US companies is expected to only grow 1.4%, a far cry from the double-digit expenditures in 2011 and 2012 (data is still being compiled for 2013, but the first half was zero). Not exactly an endorsement for robust economic activity. However, the first estimate of 2013 Q4 GDP growth is lower than Q3 but still a very decent +3.2% annualized rate, led by consumer spending and exports. However, going into the end of the month, initial January automobile sales were estimated lower by GM (-12%), Ford (-7%), and Toyota (-7%) and US manufacturing expanded less than forecast. Cold weather was blamed as the US had the first real winter in three years with snow heaped high across the Midwest, South and East Coast.

The Wall Street Journal put together this graphic comparison for the last seven years going to just before the recession in 2008. In January 2008, the US labor market reached its peak of just over 138.1 million workers on payrolls. It still has not returned to that level. Currently at 136.9 million, that number should be at 145.0 million to keep pace with population growth and to maintain the same labor force participation rate (see the graph on the right for the fall in the participation. The lower participation rate also has paradoxically improved the unemployment rate by lowering its denominator as seen in the middle graph). Capital spending for 2014 by US companies is expected to only grow 1.4%, a far cry from the double-digit expenditures in 2011 and 2012 (data is still being compiled for 2013, but the first half was zero). Not exactly an endorsement for robust economic activity. However, the first estimate of 2013 Q4 GDP growth is lower than Q3 but still a very decent +3.2% annualized rate, led by consumer spending and exports. However, going into the end of the month, initial January automobile sales were estimated lower by GM (-12%), Ford (-7%), and Toyota (-7%) and US manufacturing expanded less than forecast. Cold weather was blamed as the US had the first real winter in three years with snow heaped high across the Midwest, South and East Coast.

There was little noise from the US government in January. As expected, Dr. Janet Yellen took over as the Federal Reserve Chair from Dr. Benjamin Bernanke. As the co-architect of the easy rate policy and the taper, she will continue both. Bernanke lowered the monthly buying rate of US Treasury bonds and mortgages by another $10 billion in his last Fed meeting in mid-January. At $65 billion a month total ($35 billion in Treasuries), the Fed is still buying almost 80% of the 2014 US government debt issuance. I expect that the tapering will continue, and the monetization of the US deficit will become marginally less economically distortive. The real question is whether the debt that is on the Fed’s balance sheet will be maintained via reinvestment of interest and dividends, or allowed to mature and “roll off.” To be clear, I believe that the Fed will not sell its assets anytime soon, if ever, as that would lock in an economic loss and be bad politics. After the halt in buying, the question will be whether to maintain, not disgorge the balance sheet. The big news on the municipal bond side is the lowering of Puerto Rico’s debt rating to Junk status (BB+) by Standard and Poor’s, just as a $2 billion offering was being sold. S&P also warned that another reduction may occur within a “couple of months” if cash flow does not improve. Puerto Rico needs to find $940 million in collateral because of the downgrade, consuming half of the above offering. The sun is not shining there.

In banking and corporate news, credit and automobiles put up some negative headlines. Fannie Mae officially warned that the stepping back of hedge funds from the housing market would be negative for prices and thus its profits. To demonstrate the thirst for yield, investors have been snapping up commercial mortgages backed by homeless shelters (albeit in Manhattan’s Chelsea neighborhood) and sub-prime auto loans ($2 billion was issued the week of January 11th and $21 billion in 2013 per the Financial Times). In banking, the US government more than doubled its demanded compensation from Bank of America for faulty mortgage sales, from $860 million to $2.1 billion. An executive, Rebecca Mairone, was also found guilty of fraud and owes personally $1.1 million based on her compensation. Smaller banks that have not paid off their TARP loans face increases in the interest they owe the US Treasury. 80 lenders owe about $2 billion, but generally are too weak to pay back or raise the money they need. In mass layoff news, Wal-Mart is firing 2,300 Sam’s Club employees and JC Penney is closing 33 stores and cutting 2,000 positions. Finally, stock market brokers tout the substantial cash balances held by corporations. However, of the non-financial members of the S&P Global 1200 Index, 32% of those firms hold 82% of the $2.8 trillion available. One firm, Apple, claims 5% of it ($146 billion). Of course it cannot do anything with this cash since it is held offshore to avoid taxes and therefore not really available for investment or hiring (or dividends). It is all part of the financial mirage.

An Olympic-Sized Morass: The vibe from Davos was that Europe is on the mend but with deflation worries due to poor demand raising its ugly head in January, Draghi had to step in and commit to promises of extraordinary measures, including the purchase of bank loans. Meanwhile, commercial mortgage-backed securities hit a new two-year high in defaults as 80% of 2013’s CMBS maturities failed to pay 100% of their principal (€2.3 billion). With €14.6 billion due to mature in 2014, the rate of default will be interesting to see. The Eurozone did have decent November retail sales increases of 1.4% but that may be due to pre-buying in advance of France’s January increase in their value added tax (note to Japan!). Eurozone unemployment is still a massive 12.1%, unchanged versus the last report. With energy costs at more than double the United States and 20% higher than China, European industry (and GDP growth and employment) will continue to suffer. Privatization plans are still on the docket, with Italy looking to raise €12 billion by selling portions of the post office, a shipbuilding firm and a number of energy-related companies (including the government’s shares in Eni). A minor scandal erupted in Greece as the state gambling monopoly was sold to Russian, Czech, Slovak and Greek investors via a Cyprus holding company (can you say “organized crime” in any of those languages?).

In the short term, low borrowing costs are keeping the European countries muddling along: in January, Portugal sold €3.2 billion of debt (half of its 2014 needs), Ireland received €3.8 billion (their first issue after leaving the Euro bailout program), Spain offloaded €16 billion in bonds (at notably lower interest cost than last year) and the French electric utility EDF sold $700 million in 100-year bonds in the US (as well as $4 billion in other maturities). January also saw Intesa Sanpaolo (Italy’s second largest bank by assets) be the first Italian bank that was able to pay back its LTRO loan of €36 billion to the ECB (LTROs were cheap three-year loans the ECB made to banks in late 2011 and early 2012 – see previous commentaries). Spanish Bank Santander doubled net profits in 2013 (though lower than expectations), partially through lower loan loss reserves. Spain posted seasonally adjusted employment growth in Q4 2013 in terms of the number employed, though the jobless rate was held at 26%. This could be real, borne out of the reform of labor laws that make it easier and cheaper to fire workers. However, 90% of the created jobs were temporary or part-time contracts, so the conversion to full-time and full-benefit remains to be seen.

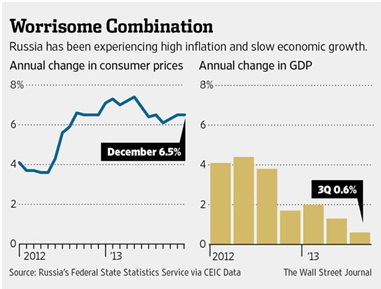

On the downside, Germany’s economy grew only +0.4% in 2013, down from +0.7% in 2012. Deutschebank confessed to losing €1 billion in Q4 2013 from trading, litigation and restructuring costs. It still has €2.3 billion in litigation reserves but JP Morgan estimates that it needs another €1.5 billion in 2014. As scandal swirls around LIBOR and foreign exchange price-fixing, DB is pulling out of the setting of London gold and silver benchmarks. Its seats are for sale, if interested (approximately costing £200,000). Germany also saw its green energy firm Prokon file for bankruptcy, hitting retail investors with €1 billion in bond losses.  I guess those investors saw red in the end. Not all Italian banks are flush with cash as Banco Populare announced a €1.5 billion rights issue to raise more equity capital before the ECB stress tests. Not a good sign for future loan losses. Barclays Bank announced plans to close 25% of its 1600 branches and lay off not only the associated workers but also an additional 400 redundancies in investment banking staff as it looks to cut £1.7 billion in costs by the end of 2014. Russia may be hosting the Olympics (and blowing tens of billions on corruption, spyware and incomplete facilities) but it is suffering from stagflation as GDP growth slowed to 1.4% in 2013 and inflation ranged between 6 to 7%. While the OECD expects GDP growth in 2014 to move up to 2.3%, it thinks that Russia will lag the global average. A tin metal for them. Finally, Italy is holding legal proceedings against S&P, Moody’s and Fitch (who?) for downgrading its debt in 2011, claiming that “S&P never in its ratings pointed out Italy’s history, art or landscape which, as universally recognized, are the basis of its economic strength.” If that is the basis for a €234 billion lawsuit, I am readying a bid for Florence.

I guess those investors saw red in the end. Not all Italian banks are flush with cash as Banco Populare announced a €1.5 billion rights issue to raise more equity capital before the ECB stress tests. Not a good sign for future loan losses. Barclays Bank announced plans to close 25% of its 1600 branches and lay off not only the associated workers but also an additional 400 redundancies in investment banking staff as it looks to cut £1.7 billion in costs by the end of 2014. Russia may be hosting the Olympics (and blowing tens of billions on corruption, spyware and incomplete facilities) but it is suffering from stagflation as GDP growth slowed to 1.4% in 2013 and inflation ranged between 6 to 7%. While the OECD expects GDP growth in 2014 to move up to 2.3%, it thinks that Russia will lag the global average. A tin metal for them. Finally, Italy is holding legal proceedings against S&P, Moody’s and Fitch (who?) for downgrading its debt in 2011, claiming that “S&P never in its ratings pointed out Italy’s history, art or landscape which, as universally recognized, are the basis of its economic strength.” If that is the basis for a €234 billion lawsuit, I am readying a bid for Florence.

All That Glitters Is Not Credit: While the naming of the Chinese $500 million investment trust “Credit Equals Gold #1” was a bit unfortunate, it was a reminder that off-balance loans always come back to bite banks and often the government, somehow. Diversification should also be a lesson as the trust invested only in one company – a coal miner. The size of the trust may be modest versus the $1.2 trillion trust market, but with $661 billion of trust loans coming due in 2014, a failure here would have reverberated through the market. 30% of Chinese credit is made through this “shadow banking” system at the end of 2013, up from 23% in 2012, demonstrating the growing reliance of Chinese industry on this funding mechanism. In the end, trust holders have been offered a deal to receive back their principal but forgo additional interest. Given they made a 10% yield for the last two years versus the 3% available from savings accounts, it seems that investors dodged a bullet.  With more trusts coming due (and yes, in the coal mining industry), this issue will continue to command headlines. On a macro perspective, the Chinese news was not particularly positive with weaker exports in December for the first time in six months. Manufacturing indices also became less positive (e.g. the official PMI fell from 51.4 in November to 51.0 in December while the HSBC January PMI shows a contraction at 49.6). 2013 statistics show GDP growth of 7.7% – a great showing for most economies but not one that will assuage fears of deceleration in the world’s second largest economy. Automobile sales are still very strong, growing 16% to 18 million units in 2013. Of the other large markets, only the US grew as mentioned above – India and Brazil both fell in 2013. China also passed the US in terms of the amount of merchandise trade, breaking $4 trillion, with the US falling shy of that level. Certainly they are still moving a lot of goods, no matter the headlines.

With more trusts coming due (and yes, in the coal mining industry), this issue will continue to command headlines. On a macro perspective, the Chinese news was not particularly positive with weaker exports in December for the first time in six months. Manufacturing indices also became less positive (e.g. the official PMI fell from 51.4 in November to 51.0 in December while the HSBC January PMI shows a contraction at 49.6). 2013 statistics show GDP growth of 7.7% – a great showing for most economies but not one that will assuage fears of deceleration in the world’s second largest economy. Automobile sales are still very strong, growing 16% to 18 million units in 2013. Of the other large markets, only the US grew as mentioned above – India and Brazil both fell in 2013. China also passed the US in terms of the amount of merchandise trade, breaking $4 trillion, with the US falling shy of that level. Certainly they are still moving a lot of goods, no matter the headlines.

Japan saw the end of an era with Sony selling or shuttering the computers and television divisions, some of the iconic consumer products associated with its brand. After being downgraded to junk status by Moody’s, radical restructuring was obviously required. Meanwhile Japan recorded its worst annual trade deficit on record of ¥11.5 trillion ($112 billion), double the deficit of 2012. Between paying record prices for fuel because of the shutdown of the nuclear power industry and a sluggish export market despite the weaker yen, the island nation continues to hope that its flawed Abe-nomics QE policy will start working before the massive sales tax increase kicks in come April. At least machinery orders are on an all-time high, showing business investment is still occurring. Of course in a country with an aging and declining population, replacing vanishing labor with capital is logical. India revised its 2012 and 2013 GDP growth rates, which highlighted the recent slowdown in its economy. As inflation kicked in at just about 10% in 2013, Raghuram Rajan, the country’s new central banker, decided to raise overnight interest rates by 0.25% to 8%, despite the potential for further slowdown. Next door, Pakistan is facing a financial turning point as the head of its central bank quit for “personal reasons.” Could it be because they suffer from 9%+ inflation and dwindling currency reserves? Indonesia finalized a $4 billion bond, its largest, but had to offer almost double the yield as last April (nine months makes a difference!) for a similar duration. Thailand is still in political turmoil as the government has declared a state of emergency with protesters closing down parts of the capital. A collapse in rice prices is adding to the tension as farmers are looking for relief from collapsing incomes.

Emerging Market Cry For Help: In addition to India above, a series of emerging market economies that play key roles in the commodities markets announced interest rate hikes or suffered other macroeconomic crises. Argentina, the poster child of default, had its currency collapse 15% in January (which had already slid by 10% since October) as its central bank halted the foreign exchange interventions that had been propping up its currency. With unofficial inflation running at 20%+ for the last few years, slow GDP growth (1.5% projected for 2014 per the FT) and farmers reluctant to export their soybeans and other crops at the unattractive official exchange rate, Argentina faces memories of the inflation last seen in the 1970s and ‘80s (12,000% and 300% monthly spikes). Given that the Presidente-for-life Christina Kirchner depends on directed subsidies and government spending to maintain power, this slide could threaten her system of political patronage. Turkey in a surprise move on January 28th increased their benchmark overnight rate to 12% from 7.75% to try to stabilize the Lira, which had fallen about 10% in the last three months. South Africa increased its lending rate by half a percent, again to combat currency runs, its first increase in six years. Finally, Libya was able to start exporting some meaningful volumes of oil but with the Eastern half of the country is still semi-independent and totally defiant against the central government, the volatile situation since the fall of Kaddafi continues.

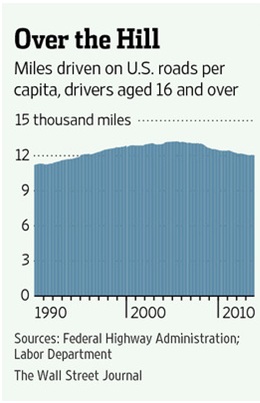

Turning to commodities and commodity companies, crude oil had some notable infrastructure news that will affect the continued low prices seen in the US and North America.  The Keystone XL pipeline (which connects Canada to Cushing, Oklahoma, the delivery point for the benchmark WTI crude oil contract) received an endorsement from the US Department of State, removing the last hurdle in front of Obama’s decision. Signing off would further hurt his relations with the environmental wing of his party, but help with the union / jobs faction, so not an easy decision for him. It would also ensure that the US had direct access to Canadian oil instead of incentivizing them to build a pipeline to the west coast for export to China. The oil is going to be extracted from the ground and sold, so we might as well be first in line for it. Oil product exports will be needed as miles per capita driven has been steadily declining, despite the strong auto sales mentioned earlier. The percentage of drivers has fallen as the median population age increased from 28 in 1970 to 38 in 2013, and the percentage of the population aged 20-24 that has a driver’s license decreased from 87% in 1995 to 80% in 2011. All of that adds up to more households without cars (9.2% in 2011 versus 8.7% in 2007) and fewer miles driven per capita (see right). Both of us at Coloma drive only on the weekends as we walk or take public transit to work – when we was younger, we drove to work and back daily – so we are part of the problem or solution, depending on your point of view. At least the Chinese auto market is booming so strongly that Tesla announced that it is offering its cars there (it already sells cars in Hong Kong). I guess that the wait times will be even longer now for their Model S!

The Keystone XL pipeline (which connects Canada to Cushing, Oklahoma, the delivery point for the benchmark WTI crude oil contract) received an endorsement from the US Department of State, removing the last hurdle in front of Obama’s decision. Signing off would further hurt his relations with the environmental wing of his party, but help with the union / jobs faction, so not an easy decision for him. It would also ensure that the US had direct access to Canadian oil instead of incentivizing them to build a pipeline to the west coast for export to China. The oil is going to be extracted from the ground and sold, so we might as well be first in line for it. Oil product exports will be needed as miles per capita driven has been steadily declining, despite the strong auto sales mentioned earlier. The percentage of drivers has fallen as the median population age increased from 28 in 1970 to 38 in 2013, and the percentage of the population aged 20-24 that has a driver’s license decreased from 87% in 1995 to 80% in 2011. All of that adds up to more households without cars (9.2% in 2011 versus 8.7% in 2007) and fewer miles driven per capita (see right). Both of us at Coloma drive only on the weekends as we walk or take public transit to work – when we was younger, we drove to work and back daily – so we are part of the problem or solution, depending on your point of view. At least the Chinese auto market is booming so strongly that Tesla announced that it is offering its cars there (it already sells cars in Hong Kong). I guess that the wait times will be even longer now for their Model S!

Of course January’s cold weather in the US has spiked natural gas and heating oil to relative highs, reminding me of the cold snap of 2003. Tight heating oil inventories due to more just-in-time inventory management from shale oil and strong exports overcame the lower dependence on heating oil as a fuel and the cost of carrying inventory is still negative, demonstrating the high demand for prompt delivery. The snow however is laying great ground cover for the row crops as well as the soil moisture buildup to avoid another drought year. Unfortunately, all that precipitation is passing California by, causing Governor Jerry Brown to declare a state emergency. Farmers have already seen 30%+ cuts in water allotment as snowpack in late January was only 12% of average for the time of year. Grains on the other hand are suffering from relative bounty as Brazilian crops have hit harvest and the boats are already steaming to China. While there is some dryness now, the soy crop, for example, is expected to be 10% larger than last year, partially from record yields. The Brazilian heat also has affected their coffee crop, sending prices higher from 113c per pound to over 135c in early February. Cocoa prices have been increasing as well as West Africa’s harvest winds down and US stockpiles decreased the last week of January. Demand is so strong that industry traders are projecting deficits for the year.

In livestock news, the most recent budget effectively bans horse-meat processing as no money was allocated for inspectors. I guess we have to send out to France for our equestrian delectables. On a more serious note, Hong Kong culled 20,000 chickens in an attempt to halt a bird flu outbreak, which has already killed two humans. Imports from southern China were blamed.  For those of you that remember those photos of the Chinese farmer with a house full of cotton (reproduced at right for those that do not), you may recall that he was hoarding his inventory during the massive run-up in prices in 2010-11. However, the Chinese government announced in January that they are abandoning their program to stockpile cotton because they bought so much that they have to dump it at a loss and end the program. By some estimates, they have as much as half the world’s stocks – and made their mills (needed for export) uncompetitive in the bargain. If you need gold, you may have to wait as Austria’s mint had to hire extra employees and add a third shift to meet demand. Finally, if you want your own commodities business, JP Morgan has theirs on the auction block with Mercuria as the front-runner. Estimated valuations run up to $6.5 billion, though some are half that. In comparison, Deutsche Bank said that it would leave the commodities markets while Morgan Stanley is selling a portion of its business to the Russian oil firm, Rosneft.

For those of you that remember those photos of the Chinese farmer with a house full of cotton (reproduced at right for those that do not), you may recall that he was hoarding his inventory during the massive run-up in prices in 2010-11. However, the Chinese government announced in January that they are abandoning their program to stockpile cotton because they bought so much that they have to dump it at a loss and end the program. By some estimates, they have as much as half the world’s stocks – and made their mills (needed for export) uncompetitive in the bargain. If you need gold, you may have to wait as Austria’s mint had to hire extra employees and add a third shift to meet demand. Finally, if you want your own commodities business, JP Morgan has theirs on the auction block with Mercuria as the front-runner. Estimated valuations run up to $6.5 billion, though some are half that. In comparison, Deutsche Bank said that it would leave the commodities markets while Morgan Stanley is selling a portion of its business to the Russian oil firm, Rosneft.

In our Bitcoin bit, the criminal enterprise Silk Road that was shut down and seized by the federal government (here in San Francisco) yielded 29,655 Bitcoins to the US Treasury. No word if they were sold or held onto as a hedge against fiat currency devaluation.

David Burkart, CFA

Coloma Capital Futures®, LLC

Special contributor to aiSource